In this article

- 1. What Does MPF Mean in Hong Kong?

- 2. Who Has to Join an MPF Scheme?

- 3. How Much Do Employers and Employees Contribute?

- 4. What Counts as Relevant Income for MPF?

- 5. When Must MPF Contributions Be Paid?

- 6. What Types of MPF Schemes Are Available?

- 7. What Changed After the MPF Offsetting Arrangement Ended?

- 8. What Happens If an Employer Does Not Follow MPF Rules?

- 9. When Can You Withdraw MPF Money?

- 10. MPF Frequently Asked Questions

The Mandatory Provident Fund, better known as MPF, is Hong Kong’s compulsory retirement savings system. It was introduced in December 2000 to help working people build savings during their employment years.

For employers, MPF is an important payroll and legal responsibility. Employees must be enrolled on time, contributions must be calculated correctly, and payments must reach the scheme trustee before the deadline. For employees, the money accumulated in an MPF account can become an important source of financial support after retirement.

What Does MPF Mean in Hong Kong?

MPF stands for Mandatory Provident Fund. It is a privately managed and fully funded contribution system regulated by the Mandatory Provident Fund Schemes Authority, commonly known as the MPFA.

Money is contributed regularly by employers, employees and eligible self-employed individuals. These contributions are invested in funds selected by the scheme member and remain in the MPF system until the person is allowed to withdraw them.

The system was created partly in response to Hong Kong’s ageing population. As people live longer and the proportion of retirees increases, personal retirement savings have become more important.

Read also: MPF vs ORSO: Understanding Retirement Options in Hong Kong

Who Has to Join an MPF Scheme?

Most employees in Hong Kong must join an MPF scheme if they:

- Are aged between 18 and 64

- Work either full-time or part-time

- Have been continuously employed for at least 60 days

Self-employed individuals in the same age group are generally required to join as well.

Some workers are exempt from MPF requirements.

| Exempt category | Common example |

| People covered by statutory pension schemes | Civil servants and certain subsidised school teachers |

| Members of exempt ORSO schemes | Employees covered by an approved occupational retirement scheme |

| Certain overseas employees | Expatriates working in Hong Kong for 13 months or less |

| Domestic employees | Foreign domestic helpers |

| Other exempt workers | Self-employed hawkers and certain EU Office employees |

Casual employees working in the construction or catering industries are covered by separate industry scheme rules and may need to be enrolled from their first day of work.

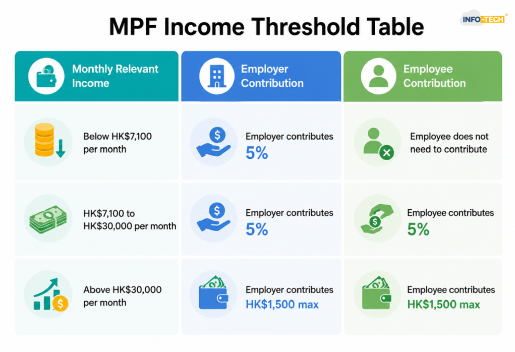

How Much Do Employers and Employees Contribute?

Employers and employees normally contribute 5% of the employee’s relevant income.

The amount depends on the employee’s monthly earnings.

| Monthly relevant income | Employer contribution | Employee contribution |

| Below HK$7,100 | 5% | No mandatory contribution |

| HK$7,100 to HK$30,000 | 5% | 5% |

| Above HK$30,000 | HK$1,500 | HK$1,500 |

The maximum mandatory contribution is therefore HK$1,500 per month from the employer and HK$1,500 from the employee.

Self-employed individuals also contribute 5% of their assessable income, subject to the applicable minimum and maximum income levels. Their maximum mandatory contribution is HK$18,000 a year.

Employees and employers may also make voluntary contributions on top of the mandatory amount.

Read also: Monthly Contribution Payment (MCP): MPF Calculation Guide

What Counts as Relevant Income for MPF?

Relevant income covers most payments an employee receives for their work. It is not limited to basic salary.

It may include:

- Salary and wages

- Commission

- Bonuses

- Overtime payments

- Annual leave, sick leave and long service payment

- Housing, travel and meal allowances

- Gratuities and tips distributed by the employer

- Double pay or 13th-month payments

Employers should look at how a payment is described and provided under the employment arrangement. Some payments may require closer review, especially where a bonus is discretionary or not directly connected with the employee’s work.

Read also: Know MPF Updates & Reforms in 2026: A Crucial Guide

When Must MPF Contributions Be Paid?

For employees paid monthly, MPF contributions are normally due by the 10th day of the following month. When the 10th falls on a Saturday, Sunday, public holiday or a day when the eMPF Platform is unavailable, the deadline moves to the next working day.

Employers must enrol eligible employees within the first 60 days of employment.

The employer’s contribution starts from the employee’s first day of work. Employees, however, receive a contribution holiday covering:

- Their first 30 days of employment

- Any incomplete payroll period immediately following those 30 days

This contribution holiday only applies to the employee’s portion. The employer must still make contributions from the employee’s first day.

What Types of MPF Schemes Are Available?

Hong Kong has three main types of MPF schemes.

Master Trust Schemes are the most widely used. They accept contributions from different employers, employees, self-employed people and voluntary contributors. They are particularly common among small and medium-sized businesses.

Employer-Sponsored Schemes are established for employees of a particular employer. They are usually used by larger organizations with a substantial workforce.

Industry Schemes are designed for casual employees in the construction and catering industries. Workers can continue using the same MPF account when moving between participating employers within the industry.

Within these schemes, members may usually choose from equity, mixed-asset, bond, guaranteed and conservative funds. Each option comes with a different level of investment risk and potential return.

Read also: Types of MPF Schemes

What Changed After the MPF Offsetting Arrangement Ended?

Hong Kong abolished the MPF offsetting arrangement on 1 May 2025.

Before that date, employers could use benefits arising from their mandatory MPF contributions to offset part of an employee’s statutory severance payment or long service payment.

For employment after 1 May 2025, employers can no longer use mandatory MPF contributions in this way. Severance pay and long service payments must be paid separately, allowing employees to keep more of their retirement savings.

Transitional rules apply to employees who started work before 1 May 2025 and leave after that date. The pre-transition portion of their payment may still be subject to the previous offsetting arrangement.

The government has also introduced a 25-year subsidy scheme running from 2025 to 2050 to help employers manage part of the additional cost.

What Happens If an Employer Does Not Follow MPF Rules?

MPF non-compliance can lead to surcharges, fines and, in serious cases, imprisonment.

Possible consequences include:

- A 5% surcharge on late or unpaid contributions

- Fines for failing to enrol eligible employees

- Penalties for deducting an employee’s contribution but not paying it to the trustee

- Fines for failing to report an employee’s termination

- Prosecution for providing false or misleading information

Failure to enrol an eligible employee can result in a fine of up to HK$350,000 and three years’ imprisonment. Deducting contributions without remitting them can carry even heavier penalties.

Employers should keep complete payroll records, contribution calculations, payment evidence and employee enrolment documents. This is where a payroll software can be of help. Payroll software by Info-Tech can calculate MPF contributions automatically using each employee’s relevant income, applying the correct 5% rate, minimum income threshold and HK$1,500 monthly cap. It can also handle changing salaries, bonuses, unpaid leave and the employee contribution holiday for new hires, reducing the risk of incorrect deductions or manual calculation errors. Contact us to stay compliant.

Read also: MPF: Essential Tips for Your Organization in Hong Kong

When Can You Withdraw MPF Money?

MPF savings are generally preserved until the scheme member reaches the age of 65.

Early withdrawal is only allowed in certain situations, including:

- Early retirement at age 60

- Permanent departure from Hong Kong

- Total incapacity

- Terminal illness

- A small balance below HK$5,000, provided no contributions were made during the previous 12 months

- Death, in which case the benefits are handled as part of the member’s estate

A person claiming permanent departure must make the required statutory declaration and confirm that they do not intend to return to Hong Kong for employment or residence.

Changing jobs does not allow an employee to withdraw their savings. The money can remain in a personal account or be transferred to another MPF scheme. Employees who have worked for several employers may also consolidate their personal accounts to make them easier to manage.

MPF Frequently Asked Questions

How is MPF calculated?

MPF is generally calculated at 5% of an employee’s relevant income from both the employer and the employee. Employees earning below HK$7,100 a month do not contribute, while contributions are capped at HK$1,500 per month for each party when income exceeds HK$30,000.

At what age can MPF be retrieved?

MPF can generally be withdrawn when a scheme member reaches 65 years old. It may be withdrawn from age 60 for early retirement, provided the person has stopped all employment and self-employment.

How much money do you get in retirement with an MPF?

There is no fixed MPF retirement amount; you receive the total balance accumulated from employer and employee contributions, voluntary contributions, and investment returns. The final amount depends on your income, contribution period, fund performance and fees, so the MPFA retirement calculator can provide a personalized estimate.

Can I withdraw my Mandatory Provident Fund (MPF)?

Yes, but MPF savings can normally be withdrawn at age 65, either as a lump sum or in instalments. Early withdrawal is only allowed in specified cases, such as retirement from age 60, permanent departure from Hong Kong, total incapacity, terminal illness, a qualifying small balance, or death.